Ever since I can remember I have felt ‘Allergic to Debt’.

As a young girl I noticed many conversations around me about people being in debt and the hardships that situation caused. I saw the strain debt put on families around me, including my own. Both my parents worked Full-Time from as early as I can remember. Five days a week, year after year, to keep up with their bills and debt repayments. However, the debt never seemed to go away, it just grew.

When I was sixteen, I started to save up for my first car. I did everything I thought was right. I worked whilst I was at school and soon enough had $5,000 saved. I paid for my own car and the repairs to get it back on the road. Then the rest of my savings went to the car registration and insurance as I couldn’t rely on my parents to help me out.

For the first six month, things were great. I was excited to finally have the freedom to drive myself to school, my exams and to see friends whenever I wanted. But I had bought a car that was 26 years old and barely 9 months after buying it, it broke down and was going to cost way more than the car was worth to fix it. I had spent all my savings on buying the car and paying for the insurance etc, so I now had nothing saved and was looking at a useless hunk of scrap metal.

For six months I car pooled with family and friends as I tried to save up as much cash as I could to get another car, but living between my Mum and my Dad’s and trying to get to TAFE and work with no car was becoming a huge chore, so I gave in and took out my first car loan for $3000 to buy another car.

Almost immediately that weekly debt repayment on my car loan started to bother me. I hated seeing that money come out of my bank account each week, taking my paycheck away from me. I was only working as a casual at the time as a Checkout Assistant at Coles, so when I got to the school holidays and I was rostered on for no shifts, anxiety hit me. I had a loan to pay and a job with hours that weren’t guaranteed.

Not long after, I decided it was time to get rid of that car loan as fast as possible. I wanted it and the stress around having a loan gone. Plus I wanted to keep my paycheck. It took me nine months of working extra shifts and paying extra on my car loan but I was finally debt-free and it felt amazing! Unfortunately, this debt-freeness didn’t last long because I was about to graduate from University with another debt to go with it.

I graduated University with $11,000 in Student Loans at just 20 years old. That may not sound like much nowadays but it was still a large number to someone who was just starting out in life. Especially when I was already trying to pay for my other expenses like board, my mobile phone, petrol and everything else.

Very quickly I realised that I still hated the idea of being in debt. For me, it just had this feeling of heaviness that I wasn’t liking one bit. I’d been here before, so I knew what to do and worked as many shifts as I was able to get between my now two jobs so I could pay out that loan again as fast as I could. I was very lucky to score an Accounting job soon after my graduation and within a year of starting my full-time job, I was able to pay off my Student Loans in full. I was again completely debt-free and so relieved!

I would love to say I never took on any consumer debt again from this point in my life but that isn’t true.

By my mid-20s I took on another car loan with the intention of paying it off in 12 months (which I did :)) and also took on $42,000 of Student Loans when I married my husband a couple of years later.

It would take us 6 years to pay off that $42,000 in Student Loans. Thankfully it was the last of our consumer debt. When we paid off those Student Loans in 2017 I knew that was the last time I ever wanted to take on another debt payment in my life (excluding my mortgage payment – but that was next to go!).

I’ve always had a bad feeling when I was in debt – that I was trapped and bound by someone else’s terms. There was no freedom. I was stuck paying those loans off regardless of what financial difficulties I might face and with a big goal to buy my first home in the not too distant future. I was now keen to stay out of debt for good.

Fast forward a few years and I am now in my early 30s (or is it mid now?? Shh!) and well aware of my ‘Allergy to Debt‘. Now that I am well into adulting, I can clarify why being in debt is not great in the long run and hopefully with the below list of reasons why I am allergic to debt, I can inspire you to do what you can to become debt-free (and stay that way) as well.

Debt may not be a ‘big deal’ but it certainly makes making ends meet a lot harder, particularly in hard times like when facing job loss, starting a family or losing an income.

Here’s 9 Reasons Why I’m Allergic to Debt and refuse to borrow money ever again (at least outside of a mortgage)! This list has grown over the years as I learn more and more about the reasons how debt holds us back financially.

9 Reasons Why I’m Allergic to Debt

1.Being in Debt Robs You of Your Financial Future

First and foremost, having debt repayments robs you of your financial future. The most important thing with investing to build wealth is to start early. That means that you ideally want to start investing for your retirement when you are in your 20s or 30s. By age 40-50 you have lost a lot of the time you need to grow your wealth with Compound Interest. It’s never really too late to start investing, but sooner is certainly better than later.

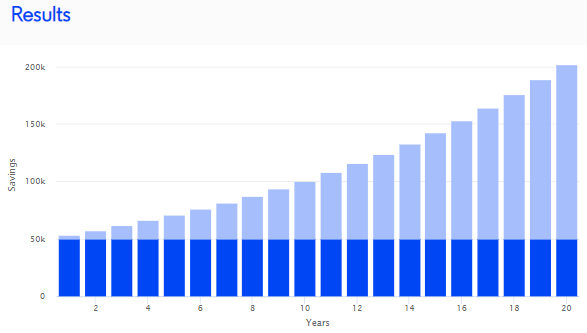

Look at this example. The first Graph shows a 30 year old who invests $50,000 for 35 years, at 7% p.a. return with no additional amounts invested after that initial $50,000. When this person is 65 they will have $600,000 in their retirement account.

In this next example, that same person didn’t start investing into their retirement at age 30 as they were tied down with debt. Instead they waited until they were 45 to invest their $50,000 so they only had 20 years to grow their investment. This person would retire at age 65 with only $200,000 – one third of the retirement of the person who put the same amount away, but 15 years earlier.

What would you rather $50k growing into $600k or $50k growing into $200k? When you put your car loan into this context that $50k loan for that fancy new car looks a lot more expensive!! Was it really such a good deal?

When it comes to investing in your future, time is money so the less money you have tied up in debt the better and more comfortable your lifestyle will be in retirement.

2. Being in Debt Allows You to Live Beyond Your Means aka ‘Fake Rich’

There are people all around us living beyond their means with the help of credit as Chris Hogan says ‘Fake Rich‘. You see the new college graduates with $60,000 salaries rocking up to work with their new $50,000 car, or young families buying $1 million properties leaving themselves in debt up to their eyeballs. You ask yourself how did they afford that? More often than not the answer is with Debt. Sure some of them genuinely can afford what they have, but not everyone.

With social media, where people are constantly sharing all the things they have bought; the nice home, the best makeup brands, the latest runners or technology gadgets it can be easy to feel left out with your average rented home and runabout car on your average salary. Soon enough we all want to keep up with the Kardashian’s and the temptation to take on debt in order to fit in with our peers is real.

The problem is, most of these people are living beyond their means and could never afford these things if they had to pay for them with their actual paycheck. It might seem like a dream come true to be able to have things that you can’t afford, but that dream can quickly turn into a nightmare.

The average minimum Credit Card repayment is only around 2% of the balance so just imagine the world of trouble people who keep charging purchases on their Credit Card are going to have when they no longer can afford the monthly repayment. Usually, by the time it catches up with people if they lose their job, or are facing an illness the financial hole they have dug themselves is too big to get out of.

I’m allergic to debt because I want to know that I can afford my lifestyle and am living within my means. I prefer to know that if anything happens to my health, my job etc, I don’t have debt repayments to maintain at a time when I need to focus on other things like my health or family.

3. Debt is Expensive

We’ve all been in this scenario. We are out shopping and see something we really want on sale. It’s such a bargain that we’d be crazy not to buy it. But we easily forget, most Credit Cards charge exorbitant interest rates, some over 20%. So that bargain top you bought isn’t such a bargain now when you take into account the huge Interest charges on that purchase if you don’t intend to pay off your credit card in full when the bill arrives.

A similar, but much more expensive scenario appears when you are shopping for a new car. If you finance a new car loan at the average interest rate of 6% on a $30,000 car over 7 years you are going to pay out the car cost plus another $6814 in interest to the financial provider over that 7 year period. That’s more than one-fifth of the value of the car!

4. Being in Debt Makes You Feel Claustrophobic

It may feel good buying that new fancy car and driving it around and showing it off to your friends and family. The first few payments might not bother you too much, it might even feel worth it when you are cruising in your car. But most car loans are now 5 or 7 years. That’s a potential 84 monthly car payments! Did you catch that? 84 month repayments! Yikes! By Payment 12 I can guarantee that debt is going to get old.

I am so ‘allergic to debt’ I go a step further to protect my paycheck, and avoid signing up for lock-in contracts so my mobile phone, TV subscriptions and gym membership are all cancel-at-anytime arrangements. A 12 month contract is long enough to plan for let alone years when it comes to a larger purchase such as a car.

5. Being Debt Free Gives You More Opportunities to Enjoy Life

When I paid off the last of my student loans it freed up a whole lot of cash for me to spend how I want. And that feeling is something I hope you all will feel one day when you are consumer debt-free. When you don’t have any more payments there are so many more opportunities that arise.

You can use your new spare cash to travel, save for your kid’s education, cut hours back a work, retire early, leave a job you hate or pick up a new expensive hobby completely guilt-free!

When you are debt-free your money is finally yours to spend how you wish on the things that add value to your life. By being allergic to debt I have been able to travel to many places in the world, pay off all my consumer debt, and dream build about my future.

6. Debt Adds Stress to Relationships

One of the biggest causes of fights between couples is money. It can be challenging to get a spender and a saver on the same page when it comes to money. Even if you are on the same page, always worrying about money can cause huge amounts of stress for you and your partner.

It doesn’t have to be this way. With each debt we paid off, we felt a sense of freedom and it felt amazing to be working towards a common goal together and our financial future. I am allergic to debt because I am not keen to ever add the complexity and stress that having debt can have on a relationship or even my own happiness ever again. It’s the #debtfreelife for this millenial.

7. Debt Makes Rainy Days Much Harder

Being in the middle of a pandemic is one of the biggest financial red flags we have seen to date. Many people have lost their job or had to take reduced hours at work. This has caused huge financial stress for many of us. Having debt might be manageable when times are good, but it can be the straw that breaks the camels back when they aren’t.

If you are facing an injury, illness or any other emergency like having to care for a loved one, having debt can make the choices you need to make much harder.

One thing I always try to accept is that rainy days happen. The less you have your money tied up in debt repayments the better it will be for you when you are trying to face those challenge without an extra layer of difficulty that debt brings. The less debt you owe, the more peace of mind you will have when life throws you lemons.

8. I Learned From Others Mistakes With Debt

I knew that I didn’t want a large amount of debt in my life from an early age. It took me a decade or two to unpack all the lessons I learned over the years from others. These have allowed me to learn valuable lessons from others without necessarily having to make the same mistakes (although of course, I too have made many financial mistakes to date!).

When I was fourteen, my Grandfather retired, aged 73. He was barely one year into retirement when he died suddenly of a heart attack. This is a memory that has stuck with me my whole life, now 20 years later. My pop worked hard his whole life and didn’t get to enjoy his retirement and spend time with his wife, children or grandchildren. I knew at 14 that I didn’t want that to happen to me. I wanted to be able to retire much younger than my Grandfather was able to so I could enjoy my retirement longer than my Pop had the chance to.

I have seen family and friends working 6 or 7 days a week to make ends meet to pay for large homes and new cars. So much so that they didn’t even have the time to enjoy their beautiful home or have much time to spend with their family. After watching others work so hard, year on year, to afford those nice things, I decided early on that having those things weren’t as important to me as my physical and mental health. I wanted time to be able to see friends, family and my husband and to have time for me. I wanted to be able to sleep soundly at night and not have to worry about a massive mortgage or car that I couldn’t afford. And it didn’t’ make sense to me to work sixty hours plus a week to pay for a home I didn’t have the time to enjoy.

For a long time these lessons impacted my thoughts around money and shaped my values and how I felt allergic to debt.

9. The Minimalist Lifestyle Made Me More Content With Less

When I discovered the Minimalist Lifestyle a few years back, this cemented my feelings about my allergy to debt even more. I realised that I could be just as happy with less. I was happy in my modest home with my regular wardrobe and affordable car. Taking on Debt to pay for things I didn’t really need or want in exchange for my physical and mental health, as well as my most valuable resource – my time – wasn’t something that I was willing to do. The price really was too high.

Well there you have it Minimisers, the reasons why I am allergic to debt. I would love to know if you can relate to any of the above at all?

Do You Want to Learn How to Spend Your Money With Intention?

If you want to take control of your financial future, stop stressing about money and learn how to spend your money with intention, book in for your free Q&A call to see how Minimise With Me Financial Coaching can help you gain clarity around your finances!

You can learn more about Minimise With Me Financial Coaching services here.

What made you realise that you were allergic to debt and motivated you to pay down your debt? Please let me know in the comments! 🙂