When I first moved out of home, I thought I had everything worked out. I could vacuum by age twelve and washed my own clothes by fourteen. And thanks to that, but the time I moved out, into my very first home at 24 but I was adulting reasonably well.

Notwithstanding that, after a few years of living out of home in my mid twentys, it became pretty evident that my husband and I were binning an unbelievable amount of food (and money!) every week.

Every Sunday, our bin collection day, came the ritual. I would open up our fridge and proceed to empty it of anything that had gone out of date or that had gone bad. Some days I would have 2-3 bags of food waste. It was all being composted by our local council, but that really wasn’t the point!

We were wasting time shopping for items we didn’t need.

My Sunday was being eaten up clearing out said fridge of our excess food, time that of course, could be better spent doing anything but clearing out our fridge accumulations. We were wasted money on food we weren’t eating and were literally throwing our money down the drain. And most importantly we were being environmentally wasteful. Perfectly good food was going in the bin because we were too time poor to cook it and often ended up just grabbing KFC on the way home instead.

Once the realisation of the level of all round waste sunk in, and the acknowledgement of the invisible money we had been throwing straight into our bin, I became extremely interested in researching the correct way to store and prolong the life of food.

Over the next couple of years I picked up heaps of tips and tricks that have helped us to Reduce Food Waste and Save Money that I am going to share with you below in the hope that it too, will help you. This list is not exhaustive, and there are many more for the different foods you consume in your household, but these are the ones that have helped me the most.

Let’s get to it, here are 15 Tips to Reduce Food Waste and Save Money

15 Tips to Reduce Food Waste and Save Money

- Shop ‘Just In Time’

Start Meal Plannning and reduce food waste and save money all at the same time without much effort! Check your calendar and shop for the meals you plan to eat at home, so you don’t end up buying more than you need. When you are more intentional with your grocery shop, not only can you reduce what ends up in your waste bin, but there are huge dollar savings to be had. Check out My Beginner’s Guide to Meal Planning here for more tips on how to shop intentionally for groceries.

nd something that isn’t touched on much, there is an awesome satisfaction to having just enough and using up what you do have. Give it a go and let me know if you found the same! 🙂

- Capsicum

Throw your capsicum in a plastic bag when you get home to make them last a good 2-3 weeks. Normally if you leave them out in the open they will start to spoil around the 5-7 day mark. Alternatively slice them up and freeze them to use on a home-made pizza or stir fry.

- Basil

I like to buy Basil plants from the local supermarket and throw them in a glass and water them each day, leaving it on my kitchen windowsill where they can get some sunlight. This usually extends the life to 2-3 weeks rather than the ones in packaging which seems to die a couple of days after they enter your fridge.

Before this I was spending $3 or more a week on basil, which seemed to always go bad when I needed it for a meal. I now can get away with spending $3 once every three weeks or as I need it.

Of course if you have a green thumb, please do grow your own, but I have tried and failed at growing it outside, but if you can you are amazing! :))

- Fresh Herbs

Reduce food waste and save money by wrapping your herbs in dry paper towel, just a thin layer underneath and on top and store your herbs in a container. We’ve done this with Coriander and it helps extend the life to at least 7 days Vs just leaving the Coriander in a container and watching it wilt in a matter of days.

Alternatively you can freeze your herbs in ice cube containers with oil to use when cooking.

- Chillies

We used to buy and bin red chillies too frequently. It was a ridiculous waste of food and money so I learnt from our extremely knowledgeable Mother In Law that you can easily freeze Chillies. Simply throw them into your freezer in the container or bag they come in and they’ll keep for months! When you are ready to use them, simply grab them out of the freezer and slice and they will defrost in your pan.

- Spinach/Rocket leaves

Another food managed to reduce food waste and save money with was spinach/rocket salad leafs. We often ended up buying more than we needed and wasting the excess until we figured out there was an easy and less wasteful way to extend the life of your Spinach or Rocket.

Like with the Herbs, mentioned earlier, if you store your Spinach or Rocket in an airtight container lined with paper towel on the top of bottom, this will draw out any moisture from the leaves, keeping them fresher for longer. This can give you extra time to enjoy your salad and save you on those costly salad bags!

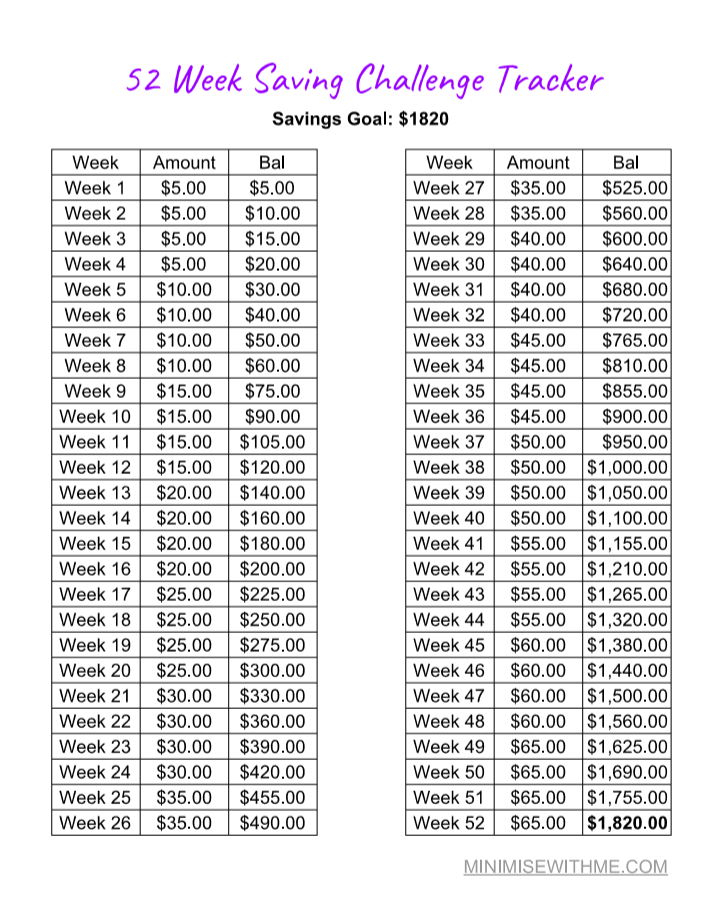

Want to Save More Money? Check out the 52 Week Savings Challenge

- Carrots

This is a super new tip I learnt to reduce food waste and save money and another easy one. I cannot tell you how many times we grabbed a kilo bag of Carrots from Aldi (as they only sell them in bulk) when we only needed 3 or 4 carrots for a soup. We’d soon forget about said Carrots and before we knew it they were bad and needed to be binned.

If this has been you up to this point, here’s an easy tip to reduce food waste and save money with your carrots..

Put all of your carrots into a large cup filled with water in the fridge. And just change out the water every 2-3 days to keep them fresh. This will make them last around 2-3 weeks! And of course you can always dice them and freeze any excess, or slice them and have them as a snack with your favourite dip!

- Bread

This is a pretty obvious one but one that can’t be forgotten. Freeze all your bread products! It’s just my husband and I so we don’t get through even a loaf a week but always like to have bread handy, so we got into the habit a long time ago of freezing everything: Crumpets, English Muffins, Bread, Wraps, Pizza Bases – you name it!

It doesn’t work so ideal for things you want to eat fresh, but for anything you plan to toast or put in the oven – it works a charm! Simply chuck in the microwave for 30-40 seconds and then toast away! And a great thing to utilise if you want to stock up on bread when it’s on sale!

- Bananas

Another tip to reduce food waste and save money is to, take your browning bananas and chuck them in your freezer for later use with baking or use them up straightaway to make your favourite Banana baked treats! My fave being banana bread. You can also use them for making Banana Ice Cream or keep them for smoothies or milkshakes!

And if you want to enjoy them for longer, simply wrap the tops of the stems firmly with cling wrap or slow down the ripening process by storing them in the fridge until the day you are ready to eat them!

- Onions

Have you ever chopped half an onion and not known what to do with the rest? Me too! An easy tip to reduce food waste and save money is to slice any left over onions and freeze them in a resealable sandwich bag. They won’t be ideal for using them fresh, but are great to throw in a curry, stir fry or on a pizza.

- Spring Onions & Leeks

I often find that I always have more spring onion than I need for my meal. Reduce waste and save money by chopping the base of the spring onion leaving about 10cm and drop the roots into a glass of water. Over the next 7 or so days you’ll have a new bunch of spring onions sprout. And surely a fun experiment for the kids!

This also works for Leaks but so far it has been less successful! I have found that around this point the base gets a bit too moist, so after this I throw it into our compost bin. But you should get two for the price of one this way 😉

With the spring onions, slice them up and freeze what you don’t need to use immediately in a zip lock back. Simply shake out the contents into your soup or stir fry when you need them and squeeze out the air in your bag when returning them to the freezer.

- Tomato Paste

If your recipe calls for 3 tablespoons of tomato paste don’t feel you need to just throw it back in the fridge, ending up with that gross mould that seems to find it’s way into the jar before you bin the jar. Divvy what’s left into an ice cube tray and store in a sandwich bag when they are frozen blocks. Pop out however many you need when you are cooking.

If you do plan to use your remaining paste in the next week or so, store the jar upside down to stop that mildew from forming inside the jar. (Just be careful not to leave if for too long as ours exploded and we had sauce everywhere ‘;))

- Eggs

If your eggs are out of date, reduce food waste and save money by testing your eggs before you throw them out. Wonder How To: Food Hacks suggests you fill a bowl with cold water and put the eggs inside. If they sink to the bottom they are fresh, if they float they are past their prime so go ahead and bin those. Rather than just binning ours the day they go over the use by date, we now do a quick check on them!

- Berries & Grapes

Another way to reduce food waste and save money is to freeze your Berries and Grapes. Taste.com recommends layering them on an oven tray to freeze and then storing them in airtight containers. The Grapes make a great frozen, healthy snack and the berries can be added to fruit smoothies!

- Celery

If you can’t quite eat a whole bunch of celery in the time it takes to go bad, try this tip from Clean My Space to reduce food waste and save money. Wrap your celery tightly in foil to keep it fresh for up to two weeks! I’ve just tested this and happy to say it certainly works! Alternatively you can dice it up and freeze it ready to use in your next batch of soup! With celery at $3-4 a bunch it’s a great way to save!

And there you have it guys, 15 Tips to Reduce Food Waste and Save Money!

This Week’s Comment Question: What do you do at home to prolong the life of you food and save money on groceries? Let me know in the comments below!

For more helpful tips to reduce food waste and save money check out:

10 Easy Tips To Save Money On your Groceries Budget and 6 Tips to Drastically Cut Your Grocery Bill!

[Photo by: Elena Koycheva @ unsplash.com]

If you found value in this post I would be super appreciative if you could share it with others who might also find value in it 🙂

![]()