A budget is a bridge between you and financial freedom. If you have no plans in place for where your money goes, it’s going to be gone just as fast as it came in. We all work hard for our money so why not take a little bit of effort to make sure all our hard work is not going to waste.

When you Create A Monthly Zero Based Budget you can spend guilt-free on what things matter to you. It doesn’t have to be this noose around your neck demanding you enjoy nothing and miss out on everything you want. If anything, a budget is the complete opposite of that. As Rachel Cruze says it ‘gives you permission to spend’, you don’t have to feel guilty about buying that coffee every morning when you know that your bills will be paid and that your savings have already been transferred across.

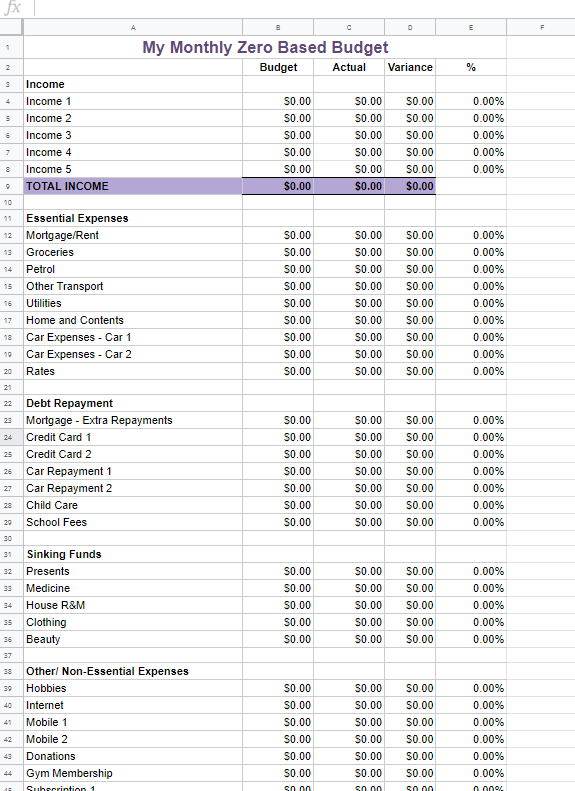

Bonus: I’ve included a link to grab your own Zero-Based Budget worksheet at the end of this post to help get you started on creating your own budget.

Rule of Thumbs

Budget Percentages Guidelines

A good rule of thumb for budgeting often shared is to Save 20%, Spend 50% and Enjoy 30%. If you have Consumer Debt you would replace the 20% Savings with 20% to Debt Repayment. However, guides and rules of thumb, are just that – a guide. Your budget should reflect your values and be completely unique to you. No two budgets will look the same!

Emergency Fund

It’s important to have an Emergency Fund which will help you create a buffer between your budget and unexpected expenses like a Dental Bill or a flat tyre. An Emergency Fund should be a minimum of $2,000, that is – enough to weather you through most storms! But of course, the sooner you can build your Emergency Fund up to 3 months of expenses, the better!

Before we start on the ‘How’ of budgeting, let’s get onto the ‘Why’ of budgeting.

Know Your Why

Before you even start your zero-based budget, you should know your ‘Why‘, that is why you want to change your finances. This is particularly important if you are trying to sell the idea to your partner. Demanding you cut all expenditure and sell everything not bolted down isn’t going to be the greatest proposal out of nowhere.

First, you must ask why do you want to work on your finances? Is it cos you work too hard to live week to week? Are you saving up for a huge goal like buying your first home or paying off your student debts? Maybe you are earning good money and spending even better money and you want to get a handle on where your money is going? Write it down somewhere and put it somewhere you can easily see it, such as your fridge.

Some of your why might be:

- To pay for our children’s future education

- To go on a trip to Disneyland

- To be mortgage-free so you can afford to work less

- To reduce stress and arguing around money with your partner

- To live a more intentional life

Once you know your motivation it’s time to start on your budget.

How to Create a Monthly Zero Based Budget

1. Put all your money on the table

Grab all payslips or anything else you need to work out what you and your partner (if you have one), earn. If you have a partner but have separate finances, do a separate budget to them. It’s up to you how you want to allocate expenses whether it be a 50/50 split or expenses are based on a percentage of income.

It’s amazing how many people can’t answer the question: what is your monthly after-tax income. We are going to change that today.

List your expected income for the month as we are going to prepare 12 budgets a year, one for each month. The cut-off date is not important, you can start it from today, or the 1st of the month. Whatever you prefer.

Calculating your income

If you are paid monthly you will only need to enter one amount for each person. If you are paid weekly or fortnightly you can put the 2-5 pays you will receive for each person. Include any other pay from second jobs, side hustles etc in their own income line.

If you have differing income payment periods that is not a problem. If you get paid $800 every Wednesday and there are four Wednesdays this month your total income for that income stream for the month would be $800 x 4 = $3200. If you have a second household salary that is paid monthly of $5000 you would add that on a separate income line to make a total income for that month would be $8200.

The following month there might be 5 Wednesdays so that month you would enter into your budget 5 x $800 = $4000 for the weekly pay plus the monthly salary of $5000 so your total income would be $9000.

Don’t forget to add in any other income that month such as bonuses, pay raises, tax refunds etc.

Budgeting for Irregular Income

If you have irregular income, so your income fluctuates, start off with the minimum you expect to earn. Base this on an average from your last three months’ pay. You might need to do some digging to get these figures.

Simply add up your total pay of the last three months and divide it by 3 and use this as your budgeting income figure. For an even more accurate minimum estimate go back six months and again, add up all income from that job and divide by 6. Total the income for the month, this is what you have to work with. This income estimate of course, will need to be reviewed regularly.

You’ll then need to base your Zero-based budget off this minimum income figure with anything extra being a bonus that you can choose to add to your Emergency Fund, add to your debt snowball to pay down debt, save it or spend it.

2. Identify your essential expenses.

It is important to prioritise your most important expenses in your zero-based budget. This ensures that you don’t go on a clothes shopping spree and leave yourself short to cover your electricity bill or groceries. You can live without a new outfit, you can’t live without food or electricity and it’s not fun not having the basics for a quality living standard. Estimate your monthly essential expenses, these might be:

- Groceries

- Electricity and gas

- Water

- Health insurance

- Mortgage or rent

- Medical prescriptions

- Child care

- House insurance

- Petrol

- Car Expenses

- Mobile

- Internet

These expenses need to come before all discretionary or debt repayments. If you can’t put fuel in the car or pay the child care bill so you can go to work you’re not going to be able to earn your income to pay any debts which is why these need to come first.

3. Set up your Sinking funds

Sinking Funds allow us to prepare ahead for things we know we need to save for in advance. Rather than waiting for November to start thinking about budgeting for Christmas, we can start allowing an amount in our budget to split the cost over 12 months. ‘The same goes for car expenses, your insurance and registration bills come every year so you need to plan ahead for them rather than stressing when the bill comes and you only have 6 weeks to find $1200!

List any items that you need to plan ahead for in your budget here. For example, if you take an annual holiday estimate your budget and put 1/12th each month away.

Some sinking fund examples are:

- Christmas

- Gifts

- Medical/Dental

- Holidays

- Home Repairs & Maintenance

- Car Maintenance

- Home Renos

- Clothing

- Beauty

- Miscellaneous expenses

Estimate the monthly cost of each Sinking Fund and list these in your budget. You might need to do a bit of math in order to make an accurate estimation. E.g. add up how many gifts you need to buy at Christmas and how much you will spend on each. Check out my Christmas Gift List Printable to get you started. And go through your car expense receipts from the prior year to estimate how much your insurance and registration will be and add in a buffer services and any unexpected repairs that are required.

A great way to track your Sinking Funds is to set them up in a separate bank account and track them with the Sinking Funds Printable or Worksheet where you can update each month how much you have put away and spent on each Sinking Fund Category and know if you are under or over budget in that category.

4. Debt and repayments

The next thing you need for your zero-based budget is to add in your debt repayments.

It is important not to think of debt as just the minimum repayment. Just because your credit card lets you pay only 2% on your debt balance doesn’t mean that you should. With that outlook, you can view debts as smaller than they are and disregard the impact the true debt has on your budget. Often people spend themselves into more debt, justified by them being able to afford the minimum repayments only to realise thousands of dollars later the financial hole you’ve dug yourself into.

The Debt Snowball Method

List all your debts excluding your mortgage from smallest to largest in a worksheet like the Debt Snowball Calculator and note the interest rate and minimum repayments. Use a debt repayment strategy such as the Debt Snowball Method to pay them down as quickly as you can. This is where you pay the minimums on all debt but the little one which you throw any spare dollars at.

Go back to your budget and mark in the total minimum monthly repayments for all debts. Then add in an additional amount for extra debt repayment. You should aim for 15-20% of your total income going to debt repayments (for all consumer debt excluding the mortgage).

Of course, if you find that your Sinking Funds and Essential Expenses are consuming all your income and you have nothing extra to throw into your Debt Snowball, this will mean you need to either cut back on expenditure or increase your income.

5. Non-essential expenses

Next, we will list the lifestyle, non-essential expenses. The things that we could live without temporarily when faced with a crisis like a job loss.

In this area we include:

- Personal Spending

- Subscriptions

- Sports/Lessons

- Entertainment

- Beauty

- Hobbies

Estimate the monthly cost of each and list in your budget.

6. Saving and investing

If you are not paying off consumer debt with the Debt Snowball (just one debt repayment method) you should be aiming to save or invest at least 10% of your pay cheque. If you can shoot for 20% even better! Pay yourself first!

If you can’t that’s something you can aim for and work towards in time, but at least mark in something for savings even if it is only $20 a week. A big part of savings is making the habit, set up your savings as an automatic transfer to come out of your pay before you even have a chance to spend it.

Balancing Your Budget

The goal with a Zero Based Budget is to ensure that every dollar is allocated to an expense or saving amount with the balance of total income less total expenses being $0. If your budget balance has gone into negative you will need to consider what you can cut from the above categories starting with the Non-Essential Expenditure. And if it is positive you can add more to Debt Repayments or Savings & Investing!

If you are short here is the time to think outside the box in order to balance the budget. Of course, it is always a good idea to find ways to save money and make more income!

Some ideas to help you balance your budget could be:

– Sell your car and pay out the loan and buy a cheaper car with cash freeing up one debt repayment

– Start Meal Planning to save in your grocery budget

– Cut your electricity bill by being more mindful of turning off power points and only using the heater and air-con on extra cold/hot days

– Pick up a side hustle to increase your income temporarily to kick start your Debt Repayment

– Bring your lunch to work and save going out with colleagues for once a week

– Ask your kids to pick one extra-curricular activity at a time until things are financially a bit less tight

– Renegotiate your interest rate on your mortgage and other debt to get interest savings

Tracking your Budget Vs Actuals

Of course, there is no point budgeting if you are going to not track it at all to make sure you stayed under budget. Make sure that you keep track of your Actual vs Budgeted expenditure each month. A great way to do this is with a PDF Printable Expense Tracker or Expense Tracker Worksheet.

Simply take note of where your money is being spent as you go and add it into your Expense Tracker. Note the Date, Store, Description of what was purchased, enter a Category and the Amount.

Add up how much you spent in each category and note it in your Zero-Based Budget worksheet ‘Actual’ column and your budget will calculate if you were under or over budget in each category and by how much.

To help you get started, click the link below to grab your free Zero-Based Budget Worksheet, so you can get started spending your money with more intention today!

This weeks comment Question: What did you cut from your budget that didn’t seem so bad once you’d made the cut? Let me know in the comments! 🙂